We don't support landscape mode yet. Please go back to portrait mode for the best experience

Six months after a Hindenburg report led to a meltdown in Adani Group stocks, the conglomerate is trying to strike a balance between growth, capex and deleveraging its debt

Gautam Adani, 61, loves business jargon. Just a few months ago, the billionaire, caught in the cross hairs of the US-based short-seller Hindenburg Research, stumbled upon a new term, ‘permacrisis’. The term, which refers to a prolonged period of uncertainty, was chosen as Collins Dictionary’s word of the year in 2022. It describes the turbulent and uncertain nature of that year, and perhaps also the situation the Adani Group’s Chairman and Founder finds himself in—as he navigates the mother of all existential crises of his three-decade entrepreneurial journey.

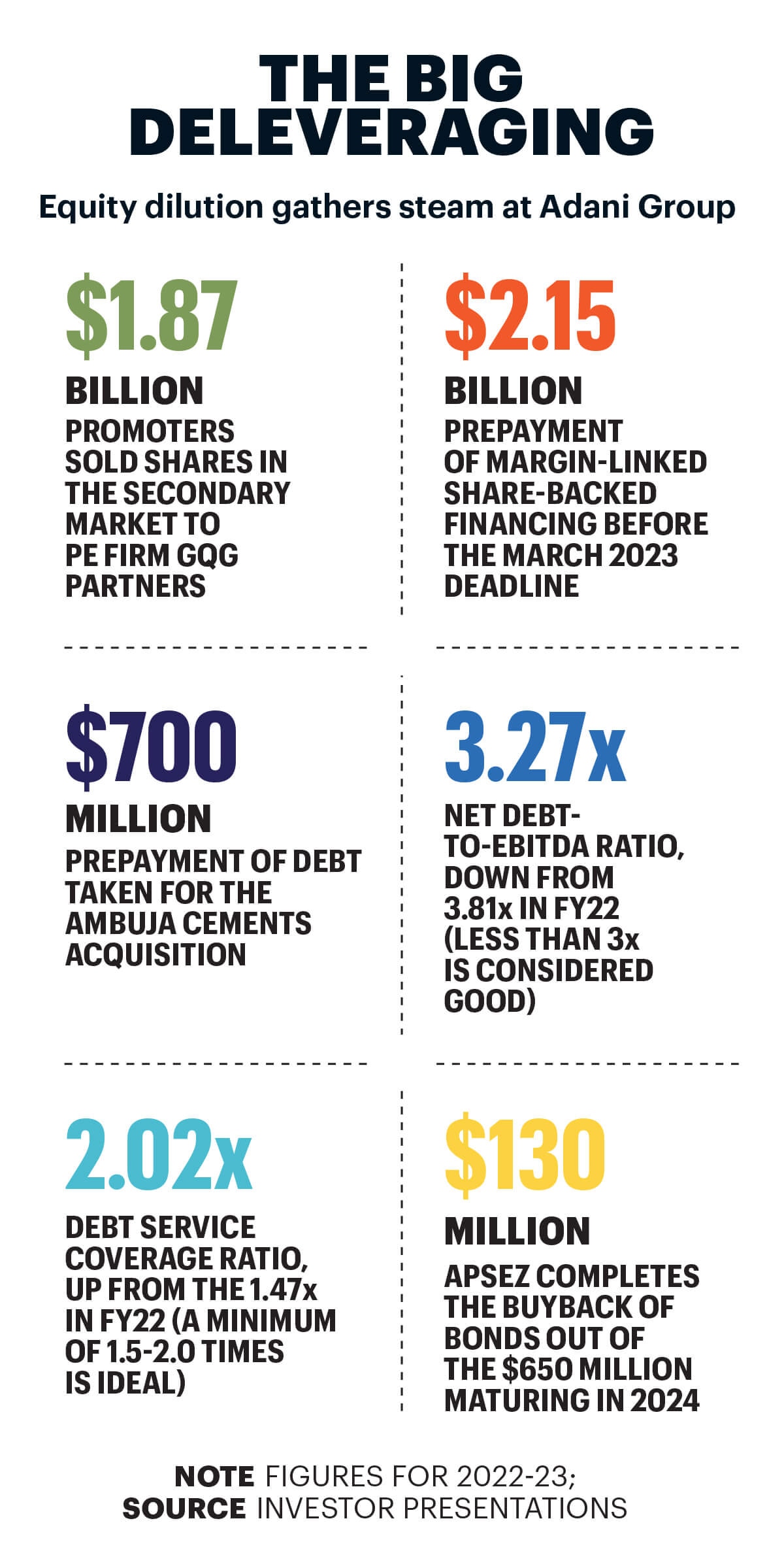

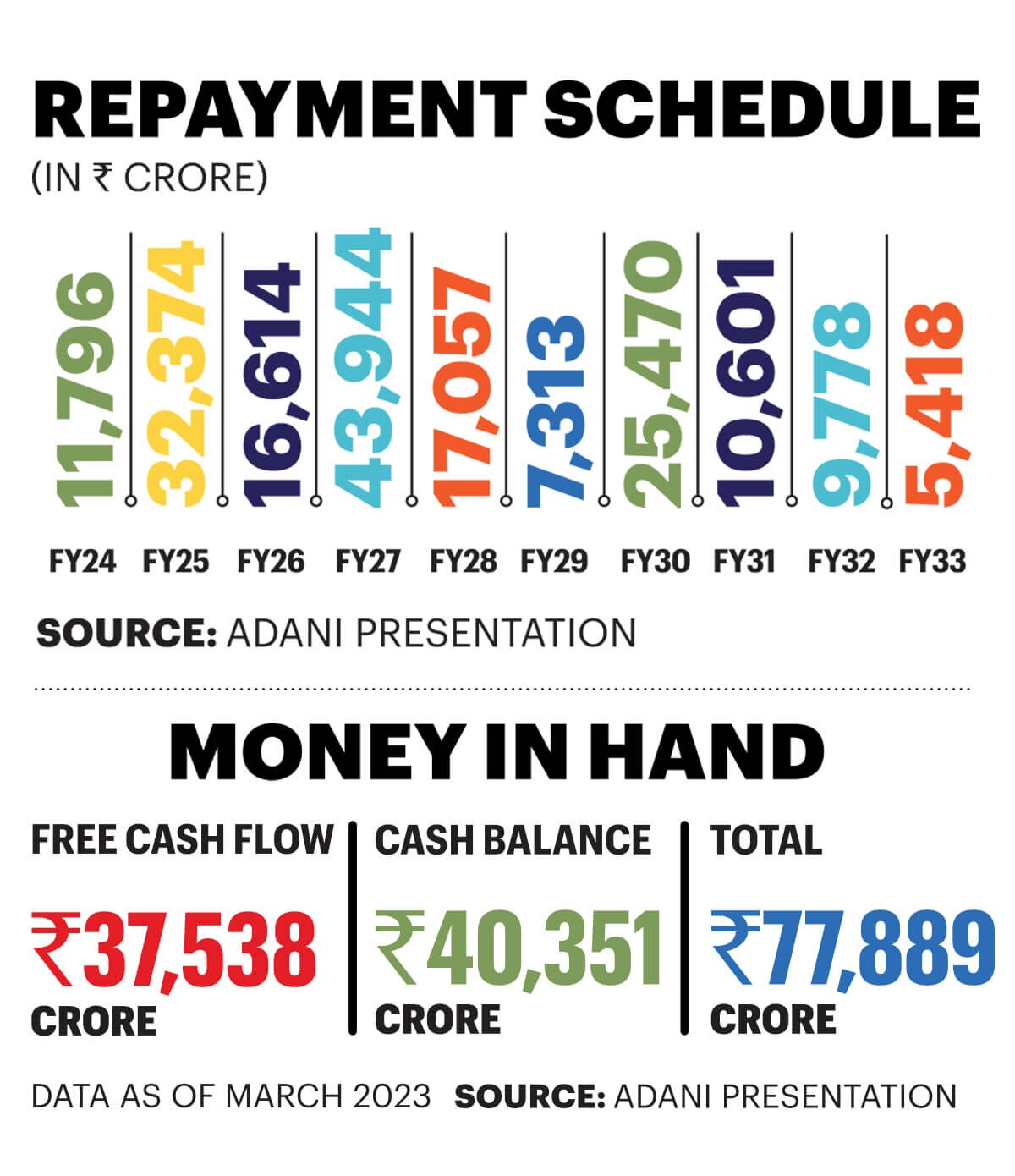

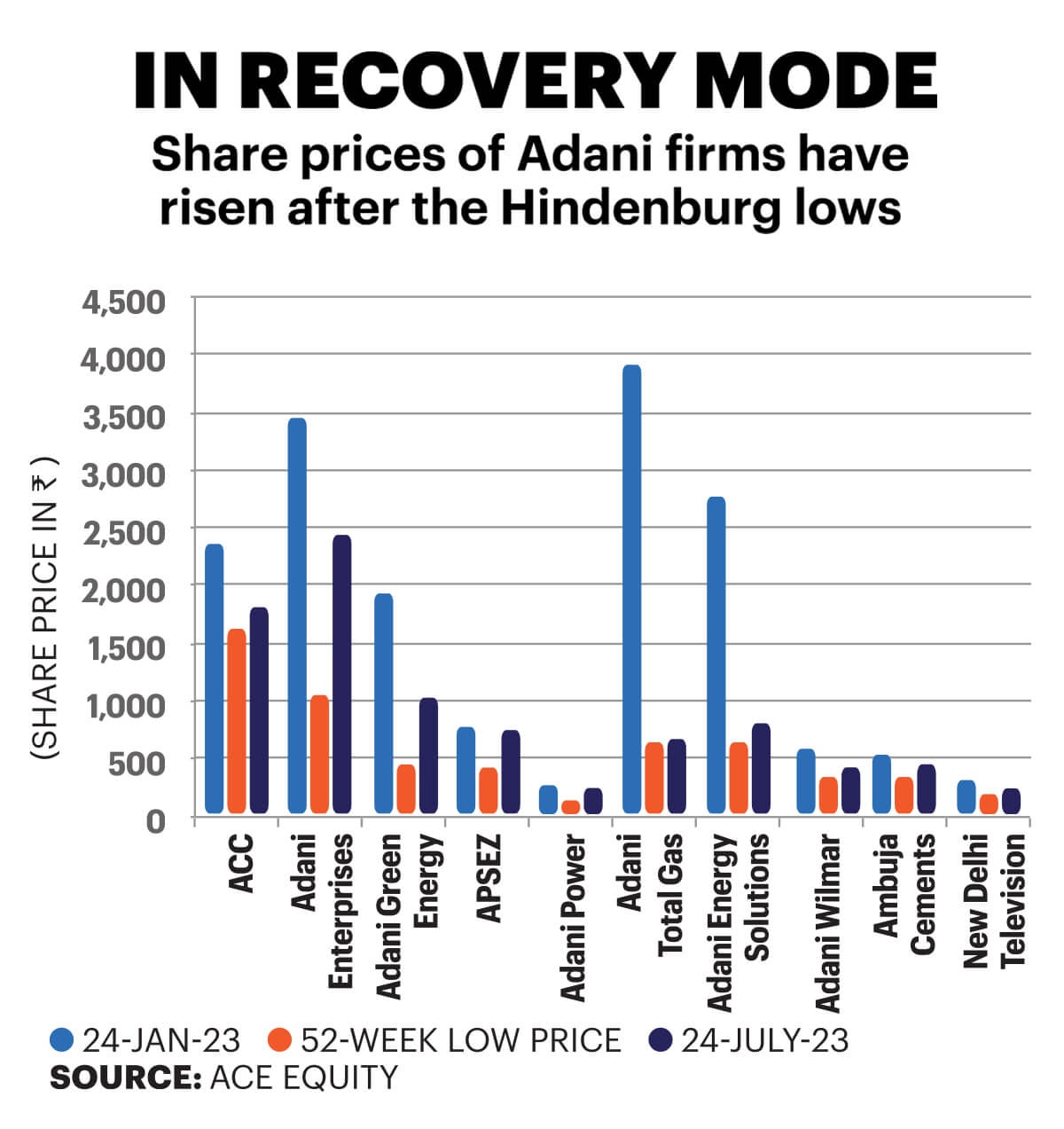

Though the challenges still linger—sparked by a Hindenburg report alleging accounting fraud, stock manipulation, and routing of funds through foreign shell companies, all of which the firm has refuted—there is some breathing space. The group, which has a top line of Rs 2.62 lakh crore and had lost over $100 billion in market capitalisation at one point, is gradually charting a new course by rebalancing its growth ambitions, slowing down on big-ticket acquisitions, deleveraging, and strengthening its balance sheet. The Adani family recently divested stakes in four group companies to raise $1.87 billion (Rs 15,500 crore) from global private equity firm GQG Partners. In addition, three companies have board approval to raise funding of $4 billion over the next 12 months. “There will be more equity dilution if they plan to grow at the same pace as earlier. It’s a Catch-22 situation. If growth slows down, the valuations will correct further,” sums up Ambareesh Baliga, a seasoned observer of the markets. But the group has been diluting equity since 2019 when global players like TotalEnergies, Qatar Investment Authority and Abu Dhabi-based IHC group invested a total of $5.79 billion.

There will be more equity dilution if they [the Adani Group] plan to grow at the same pace

as earlier. It’s a Catch-22 situation [for them]. If growth slows down, the valuations will correct furtherAmbareesh Baliga

Stock Advisor

“Over the next 20 years, Adani portfolio companies and promoters want to raise $50 billion of equity… We want to invest close to $500 billion in core infra as a base case. We will run this programme of equity for the next two decades,” says Group CFO Jugeshinder “Robbie” Singh.

But the new equity is coming with higher dilution. Besides, there are hard choices being made. For instance, the group recently exited the financial services business; it is now focussing on its core infra model, plus adjacencies. “We invest for an intergenerational period, upwards of 30 years. We have not even completed the foundation of our growth. For instance, we are setting up a ports business to be able to handle and move cargo equivalent to what India moves today as a country. We have to remain strategically patient,” explains Singh.

The firm’s equity will be recycled, as cash flow from each year serves as equity contribution for the next project. So, ROE is expected to keep expanding

Vinit Bolinjkar

Head of Research

Ventura Securities Ltd

Market watchers are taking note. Stakeholders Empowerment Services (SES), a proxy advisory firm, terms the Adani Group’s debt concerns as overstated. Rohit Chawda, acting CEO at Taurus Mutual Fund, agrees. “The current challenging period will only drive the company to make more prudent investment choices, and corporate governance standards will improve even more,” he says.

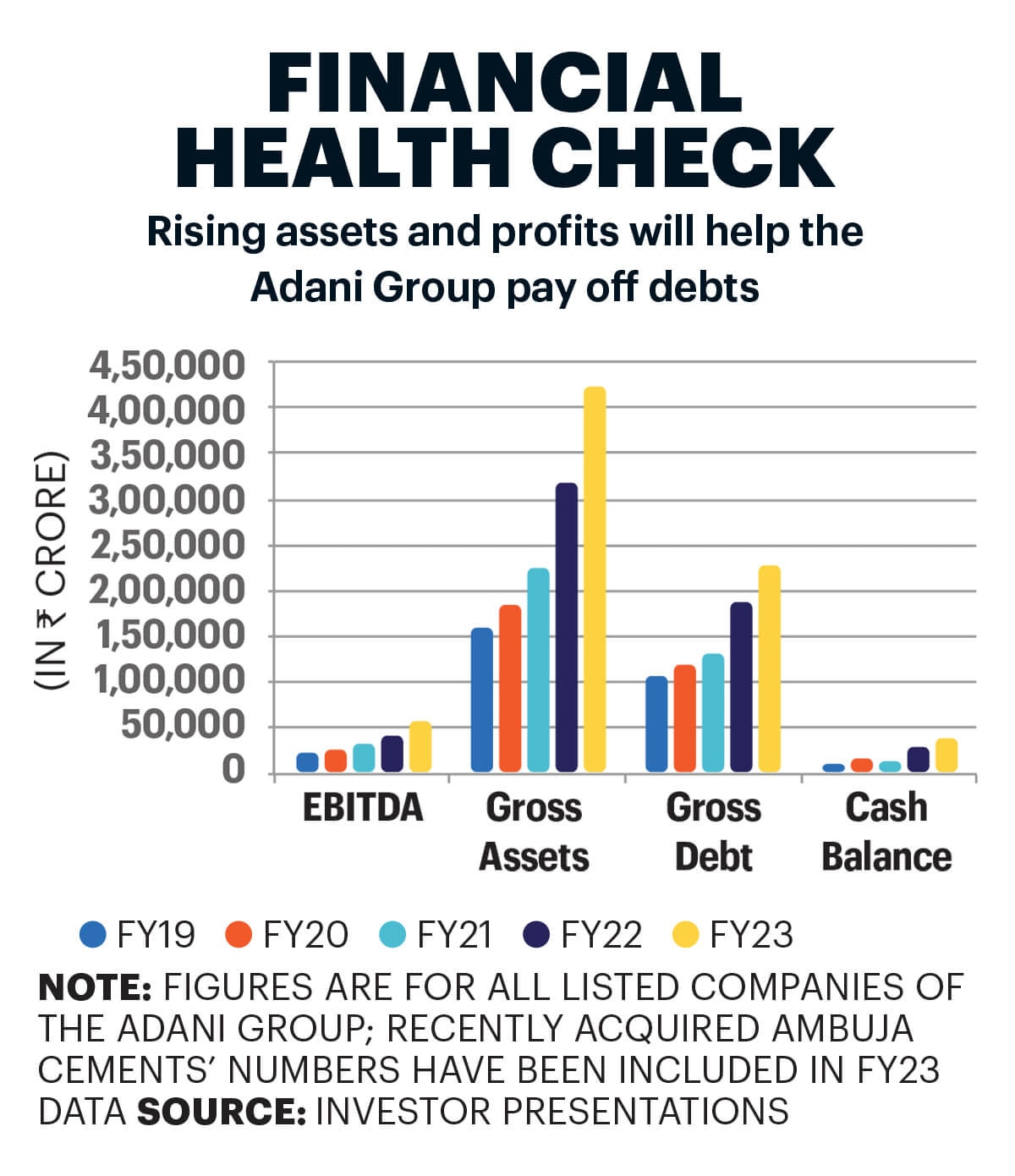

“Our balance sheet, assets, and operating cash flows continue to get stronger and are now healthier than ever before,” Gautam Adani had said while sharing the group’s operational performance with shareholders in July. His bet is on infrastructure assets, which generate stable revenues and contribute over four-fifths of the group’s Ebitda. A proxy for cash flow generation capacity, Ebitda shows the group’s core operating performance. (See box Financial Health Check.) Florida-based GQG, the group’s top backer—which is located just 1,000 miles away from Hindenburg’s New York headquarters—is estimated to have invested more than $4 billion in Adani Group companies, including from the secondary market. Rajiv Jain, Chairman and Chief Investment Officer of GQG Partners, advises the Adanis to not deleverage too much. “This is the time to go full throttle,” he says. How is Gautam Adani keeping all the balls in the air? Let us find out.

The current challenging period will only drive the company to make more prudent investment

choices, and corporate governance standards will improve even moreRohit Chawda

Acting Chief Executive Officer

Taurus Mutual Fund

Adani Enterprises Ltd (AEL), the group’s holding company that withdrew its Rs 20,000-crore follow-on public offering earlier this year, is back in the market with a Rs 12,500-crore equity raising plan. “Of the several projects underway, two of the key ones include the Navi Mumbai Airport and the copper smelter [in Gujarat’s Mundra]. Both are on schedule. The Navi Mumbai Airport is preparing for operational readiness and airport transition by December 2024,” Gautam Adani had announced to shareholders.

Then there’s the data centre business AdaniConneX, the expansion of which is on track. In June, AdaniConneX secured $213 million in financing from over half-a-dozen foreign banks. This money will be used for data projects in Chennai (with 17 MW capacity) and Noida (50 MW). It has acquired land for data centres in Navi Mumbai and Visakhapatnam, while the Noida and Hyderabad ones are almost 30 per cent complete.

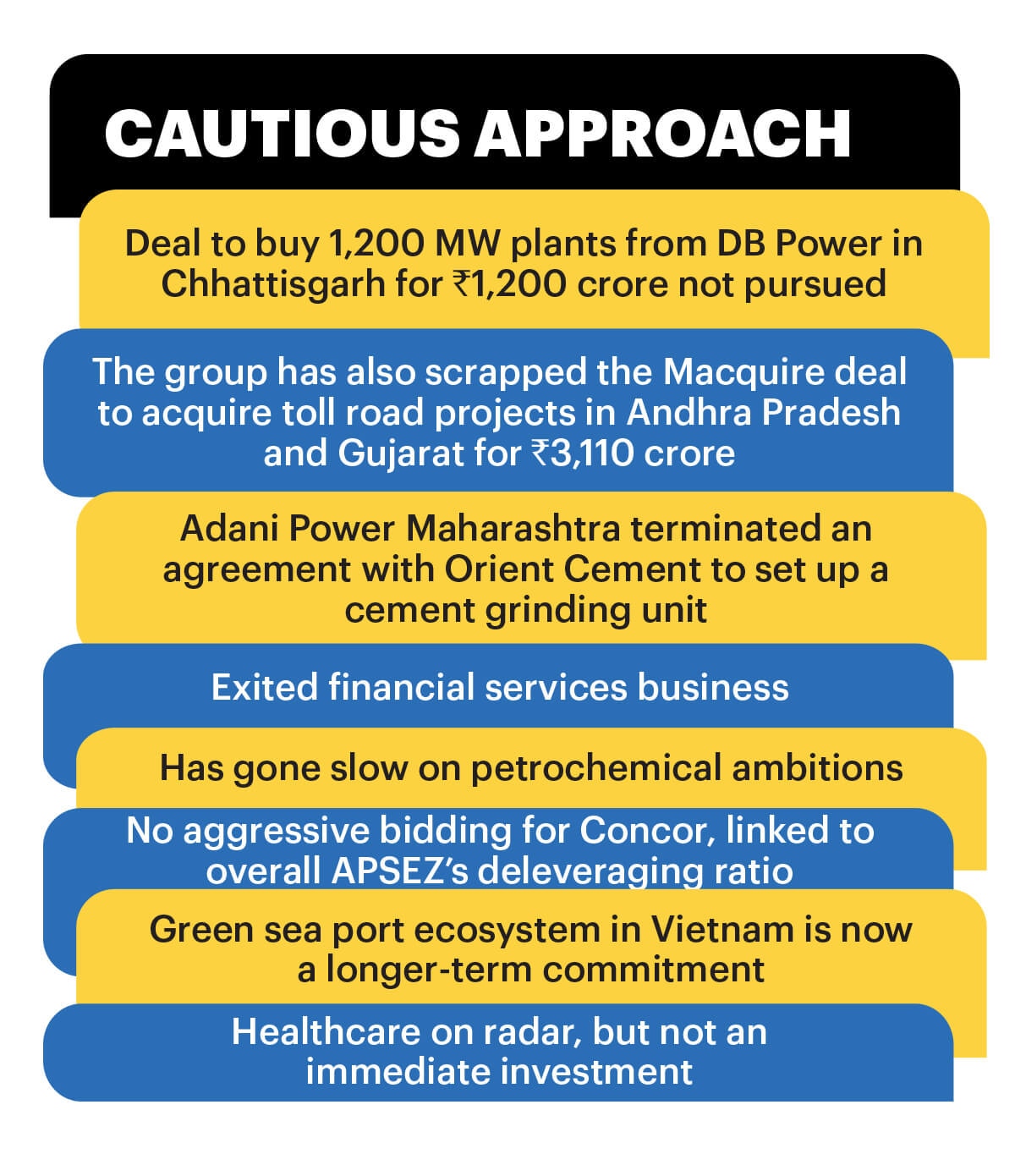

Adani Road Transport, meanwhile, remains on the sidelines of bidding for projects. The company claims that the 64-km Ganga Expressway Project in Uttar Pradesh has achieved financial closure. In June, the company with a roads portfolio of Rs 40,000 crore decided to walk out of Macquarie’s Rs 3,110-crore toll roads project deal.

AEL’s biggest bet is green hydrogen (through AEL subsidiary Adani New Industries Ltd, or ANIL), where it is setting up an ecosystem—from generation of green hydrogen, downstream products (ammonia and urea), to manufacturing of supply chain products like wind turbines, batteries, and electrolysers. CARE Ratings says the company has decided to defer the large-scale capex plan in green hydrogen till market and investment appetites have revived. There has been a downward revision in capex plans to optimise capital. “[But overall] we remain on target. ANIL is nearly mid-way through completing our integrated manufacturing facility for green hydrogen,” says Singh.

Today, Adani Green Energy Ltd (AGEL) has the largest operating renewable energy portfolio with 8.1 gigawatt (GW) of capacity, with a target of 45 GW by 2030. It plans to add 3 GW of capacity this year, matching last year’s addition. It has lined up a capex of Rs 14,000 crore, while in July the AGEL board cleared a proposal to raise Rs 12,300 crore of equity share capital. “[The] Adanis are efficient; for example, they get paid in 60 days versus 260 [days] for a competitor. Given their efficiencies, it is our view that the company will generate higher returns,” says GQG’s Jain.

In terms of revenue visibility, there is a 25-year fixed-tariff power purchase agreement (PPA) with an average portfolio tariff of Rs 2.98 per unit. Analysts, however, are wary of AGEL’s valuation, which is 32 times its book even after correction. “The company’s equity will be continuously recycled, as the cash flow generated each year will serve as an equity contribution for the next project. As a result, the return on equity is expected to keep expanding,” explains Vinit Bolinjkar, Head of Research at Ventura Securities.

Then there are potential challenges, such as if a distribution company (discom) defaults on payments. While renewable energy is the future, the thermal power business (called Adani Power Ltd or APL) is raking in profits and has made its first transnational foray by supplying power to Bangladesh. It will supply 1,496 MW of power for 25 years. APL, with an operational capacity of 14,450 MW, is aiming for 16,850 MW by June 2027.

The Adani Group is focussing on consumer-centric businesses for growth, whether it is airports, energy and gas distribution, real estate, or FMCG. Many of these are extensions of B2B businesses—for instance, the entire power chain. It has expanded from power generation to transmission to distribution.

Adani Transmission Ltd (ATL)—renamed Adani Energy Solutions recently—has lined up equity fund raise of $1.03 billion, and has planned a capex of Rs 4,500-5,000 crore in the next couple of years. It sits on a transmission network of over 15,000 circuit km (ckm), with 4,400 ckm under construction. The mandatory escrow account requirement for discoms makes it a safe business. “The money collected from consumers (B2C) by discoms is compulsorily transferred to this escrow account for paying the transmission players,” says Bolinjkar. A part of the capex will also go into the power distribution business, catering to over 12 million consumers in Mumbai and Mundra SEZ. The government is also amending the Electricity Act, which will allow for multiple distribution companies in the same geography. “The most efficient business should win. It’s the survival of the fittest, and the consumer benefits in the end with cheaper electricity and better service,” says Jain. ATL’s focus is on reducing power costs and switching from thermal to green energy. “The implementation of smart meters is expected to contribute positively to its margins,” adds Bolinjkar.

“Ultimately, distribution and metering will be a bigger part of the energy solutions business by 2028,” says Singh. Hence the renaming.

In the city gas distribution business of piped natural gas (PNG) and compressed natural gas (CNG), Adani Total Gas Ltd’s (ATGL) focus is on building pipeline networks in newer geographies. It currently has 460 CNG stations, 704,000 PNG homes, and 7,435 industrial and commercial connections. “Our company is going to build over 1,800 CNG stations in the next seven to 10 years,” said Executive Director & CEO Suresh P. Manglani in ATGL’s annual report. The investment planned is Rs 18,000-20,000 crore. “The city gas distribution business carries no cash flow risk. With a debt-to-Ebitda ratio of just 1, there is no gearing involved,” says Bolinjkar. However, the new administered pricing mechanism has now linked gas prices to crude oil. “If global oil prices soar, the company may be required to purchase gas from the spot market, which could potentially impact its ability to maintain healthy margins,” says Bolinjkar. That’s where the diversification strategy to build e-mobility and compressed gas businesses for the future fits in well.

In FMCG, Adani Wilmar is gradually reducing its reliance on edible oils (79 per cent contribution in value) in favour of food and FMCG, which includes wheat flour, rice, pulses and sugar.

Days after the Hindenburg report, Gautam Adani had landed in Israel to complete the $1.15-billion acquisition of Haifa Port. GQG’s Jain interprets it as a clear vote of confidence, reflecting the Israeli government’s trust in the group’s competence. Haifa Port’s Indian Ocean-Mediterranean route will strategically position the company. Adani Ports and Special Economic Zone (APSEZ), which handles one-fourth of the country’s cargo volumes through 14 ports, is also expected to commission India’s largest trans-shipment hub in Vizhinjam, Kerala, and a port in Colombo. It has planned a capex of Rs 4,000-4,500 crore in the current fiscal. “APSEZ is the best proxy to take part in the growing Indian economy, especially in the goods trade,” says Chawda of Taurus.

Then there’s ACC-Ambuja Cements that the group acquired last year from Switzerland’s Holcim for $10.5 billion to become India’s second-largest cement producer. In terms of expansion, it plans to double cement capacity to 140 million tonnes (MT). But first, it is taking advantage of group synergies to reduce costs. For instance, it can save Rs 300-400 per tonne from energy costs, freight costs, and forwarding costs.

Explaining the overall investment philosophy, Singh says the group currently has a portfolio of 10 companies. “We will have close to 14-15 companies by around 2033. We have an objective to hold a certain percentage in our portfolio. Within that portfolio, when we recycle capital, it is not dilution,” he says. The promoters want to own the majority and the highest stake possible in the early-stage companies. “Our objective is to get our portfolio into a position where the current cash that we hold in the bank and free cash flow is greater than any debt maturity requirement. At a portfolio level, we will get there by 2025,” he says.

While the Supreme Court-constituted expert committee on the Adani stocks crash did not find any regulatory failure, the sword of ongoing investigations by the Securities and Exchange Board of India (Sebi) is still hanging over the group’s head. “We remain confident in our governance and disclosure standards,” Gautam Adani had said, putting up a brave front before shareholders. The group’s stocks are showing a gradual recovery, and it is also expanding internationally. For instance, Adani was in Sri Lanka in July, rubbing shoulders with President Ranil Wickremesinghe. With a container terminal and a wind project already in his bag, he pitched for a green hydrogen plant.

Amidst the crisis, Gautam Adani’s greatest asset remains his management team and board, standing firmly by his side. If he successfully navigates the current challenges, he will surely write a new chapter in his entrepreneurial journey, possibly even introducing the term ‘permasuccess’ to the Collins Dictionary.

Story : Anand Adhikari

UI Developer : Pankaj Negi

Producer : Arnav Das Sharma

Creative Producer : Raj Verma

Videos : Mohsin Shaikh